Rates have remained high throughout 2021, and shippers have been anticipating the market to rebalance. They may be waiting a bit longer, as seasonal slowdowns after the holiday season may not be as dramatic as most shippers are accustomed to — and hoping for — during the first quarter of 2022.

Peak season is in full force this year, and spot rates are likely to hit their peak during the fourth quarter of 2021, according to David Spencer, Arrive Logistics’ director of business intelligence. Still, shippers should continue to expect challenging conditions come January due to a myriad of compounding challenges on the supply side of the market.

Spencer teamed up with Aaron Galer, Arrive Logistics’ senior vice president of strategic partners, to host the company’s Metrics that Matter webinar, an extension of Arrive’s monthly Market Update. The pair explored recent market trends and upcoming challenges in an effort to help shippers better understand the ever-changing logistics landscape.

The duo predicted only minor rate decreases after peak season, a stark difference from the exaggerated mid-January drop-offs shippers have grown accustomed to over the years. Any rate decreases seen in the first quarter of 2022 can be attributed to changes in demand, including slowing consumer spending, lower urgency from shippers and general seasonality.

Shifts in consumer spending are expected to drive mild rate changes in the coming months. Demand surged throughout 2021, but current consumer spending trends are not sustainable. People are saving money at rates similar to those seen before the coronavirus pandemic, and credit card spending is on the rise among Americans making less than $50,000 per year, according to data from Bank of America Global Research. This points to increasing debt levels and decreasing ability to continue spending money at current rates.

“Government stimulus money has played out, and the personal savings rate is back to the level we saw pre-COVID. As that declines, that is signaling to us that some of this has played its course, and we might start to see this increased level of spending leveling off,” Spencer said. “This is not going to result in an immediate cliff of decreased demand. There are still incredible backlogs out there, but we believe we are seeing the beginning of the consumer changes that lead to that cliff.”

On the supply side, capacity constraints are expected to remain in place throughout at least the first half of 2022 as equipment and driver shortages remain. These constraints will limit how far rates can fall in the first half of the year.

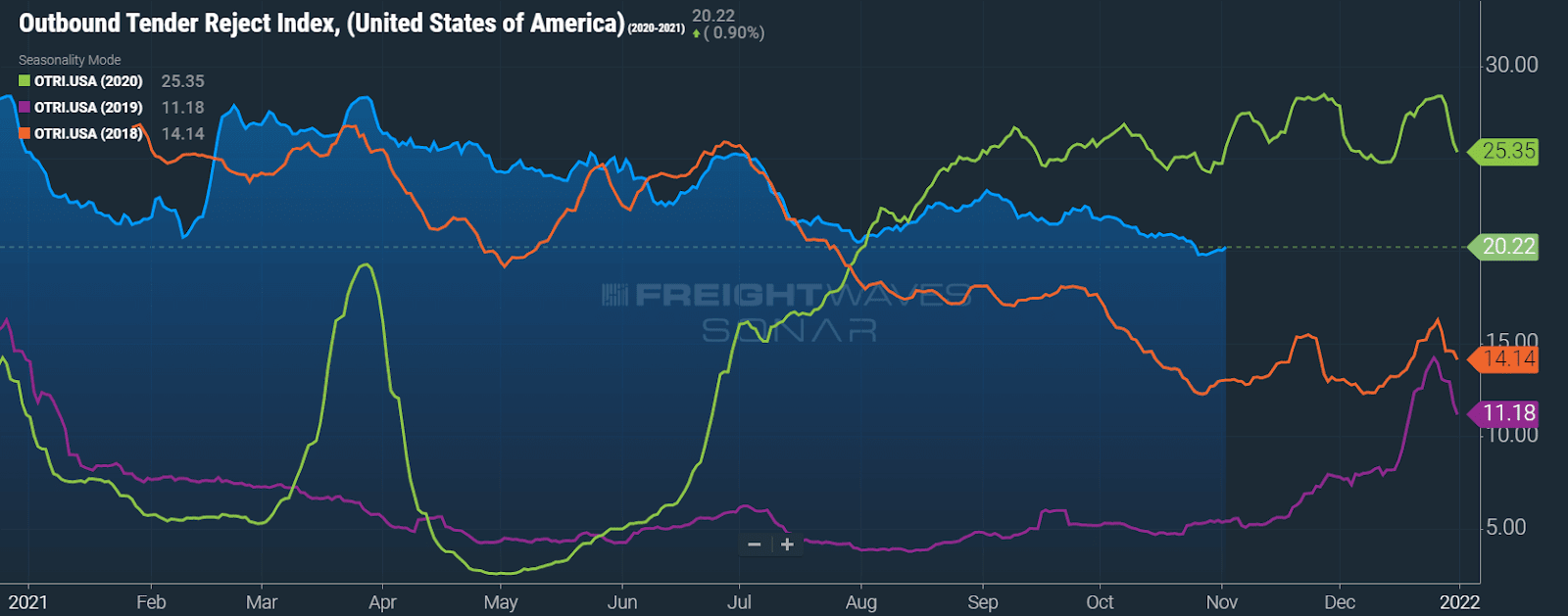

Increasing contract rates seen over the past year have prompted a small slowdown in tender rejections, according to Galer. Still, rejection rates remain above 20%. Tender rejections briefly dropped below 20% for the first time since July 2020 at the end of October 2021, according to FreightWaves’ SONAR Outbound Tender Rejection Index (OTRI). This number rose again in early November.

Despite rising contract rates, carriers continue to suffer from equipment delays and driver shortages while trying to expand to meet demand. Arrive’s recent carrier survey indicates that truck, trailer and driver delivery issues continue to be the primary factors weakening the capacity outlook, with 20% or fewer carriers claiming to be confident in their ability to find drivers or equipment.

These challenges, coupled with rising fuel costs, indicate once again that shippers should not expect to see dramatic rate decreases once peak season has subsided.

Finding capacity, however, is not the only issue facing shippers today. Not all shippers are struggling to find capacity, and many of them are no longer willing or able to settle for just any available truck. For some shippers, the current capacity crisis is less about finding trucks and more about finding acceptable service.

“There is capacity there, but the level of service they are getting for that capacity and the price that they’re paying for that level of service is just far below what their expectations are,” Galer said.

Galer further explains that this issue is, in part, due to the same issues that have caused today’s capacity constraints in the first place. Due to parts and equipment shortages, many carriers are working with aging fleets. Older trucks naturally tend to have more problems and experience more breakdowns. Being continually faced with issues like equipment breakdowns or overextended drivers makes it difficult for shippers to meet current consumer delivery expectations. This is an especially difficult realization considering current rates.

Shippers have been required to make some sacrifices due to current market conditions, but they have proven eager to innovate and evolve past these issues. They are wondering when the level of service they receive will begin to match the premium rate they are paying, and they have been quick to search for solutions.

In order to combat service issues, shippers have been moving away from the annual RFP process, according to Galer. Some shippers are holding more frequent, quarterly RFPs to save costs. Others, who may place a higher priority on service, are accepting the higher costs and committing to multi-year contracts. These shippers are supplementing them with regular bids to patch their networks as carriers fall off and in return, experience fewer service failures.

Both of these unique approaches allow shippers an added layer of flexibility and security when it comes to moving their goods at competitive rates without compromising customer service. Revisiting RFPs on a more frequent basis allows shippers to respond to market changes in real-time while locking in expanded RFP’s offers some protection against future rate hikes.

One thing is clear: Shippers will be called on to continue innovating in 2022.